Amidst the collapse of Bear Stearns and the bailout of AIG, it’s easy to forget about the federal government’s hand in creating the 2008 recession. Back in the 1990s, Barney Frank, with the help of the United States Department of Housing and Development, decided to raise Fannie Mae’s quota for purchasing loans from low income buyers. Over the course of about 15 years, from 1992-2007, these rates jumped from 30% to 55%. By the early 2000s, Fannie Mae was offering no-down payment loans and had bought over a trillion dollars in subprime mortgages. Of the 27 million outstanding subprime loans during the 2007 crisis, 70% were owned by the federal government.

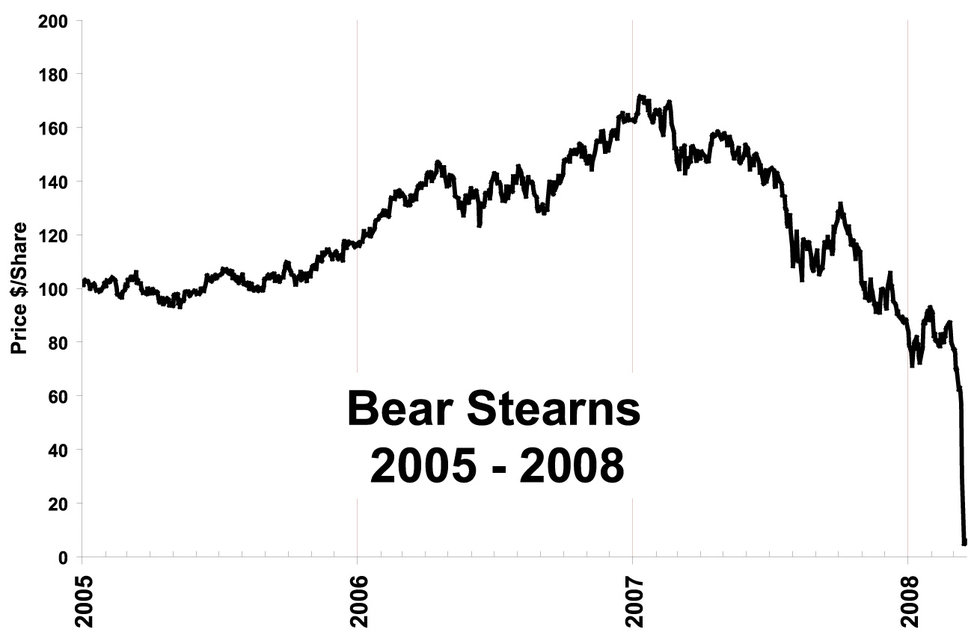

The sudden fall of Bear Stearns’ stock

The sudden fall of Bear Stearns’ stock

Last year, Fannie Mae and Freddie Mac redefined the term subprime, lowering the credit threshold for what constitutes poor credit from 660 to 620, almost as if these agencies suddenly contracted amnesia. To make matters worse, the Federal Housing and Finance Agency’s goals are to finance loans on about 400,000 low income homes each year from 2018-2020. While these loans aren’t necessarily subprime, it’s safe to assume that a good portion of them are. On top of this, Fannie Mae has also raised their debt-to-income (DTI) ratio limit from 45% to 50%, and the share of loans with high DTIs has jumped from 6% to 20% over the past year. The argument for these incredibly lax regulations is that many people had their credits decimated in 2008 and that millennials, the newcomers to the housing market, have more debt than other generations. It makes sense for the government to help struggling people find homes, but raising the DTI threshold while lowering credit requirements for mortgage loans is one of the riskiest methods conceivable.

The private sector isn’t much better though, and investment in subprime mortgages is back; they’ve just been rebranded as nonprime (which isn’t even a real word). Some companies, like Carrington Mortgage Services in California, are offering loans to people with FICO scores as low as 500, about 250 points shy of the current average for agency-backed mortgages. Obviously, there’s a higher down payment associated with these lower credit scores, but the resurfacing of subprime loans is disturbing, particularly when a spokesman for Carrington says something like, “We believe there is actually a market today in the secondary market for people who want to buy nonprime loans.” Never mind that this isn’t a sentence, listen to what this person is saying. Banks are also latching onto this idea, and some have been known to offer mortgages for 0% down.

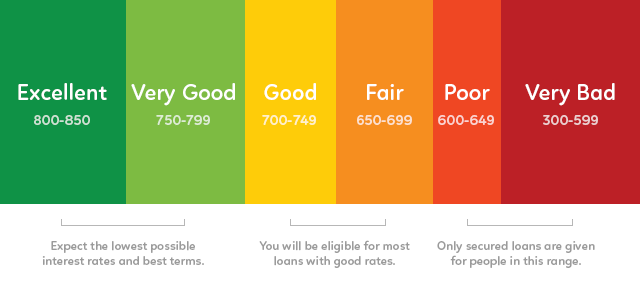

Fico credit score chart. During During the 2008 financial crash, a credit score under 650 was considered subprime.

Fico credit score chart. During During the 2008 financial crash, a credit score under 650 was considered subprime.

Another disturbing development is the current popularity of Federal Housing Administration (FHA) loans. Currently, the FHA controls 21% of the total mortgage market and 35% of loans purchased by Millennial homeowners. These loans are traditionally designed to help lower income Americans buy houses. Nowadays, their loan limits don’t necessarily reflect this. Loan limits, depending on the area, range anywhere from $294,515 to $679,650, and for buyers with a credit score of 580 or higher, these loans only require a 3.5% down payment. If someone’s credit score is between 500-579, they can purchase a home for 10% down. Even if a mortgage company tacks on a 1.5-2% fee, this gives large swaths of people with ostensibly terrible credit the option to put only $25,000 down on a $500,000 home. The DTI threshold for an FHA loan? 57%.

To compound things further, 93% of FHA loans issued in 2016 were handled by mortgage companies, not banks. These companies, for obvious reasons, are much less resistant to liquidity issues than big banks, and there is research to suggest that mortgages issued by nonbank lenders tend to be associated with much lower credit scores. Not only are these companies woefully unprepared for an uptick in delinquencies–an uptick that’s almost certain with the Fed increasing the interest rate–they’re actively selling loans to high risk candidates. In the event that homeowners default on their mortgages, there’s no way these companies can eat the cost. This is bad news for the Government National Mortgage Association (Ginnie Mae), the agency that manages and insures the FHA. While lenders dealing in FHA loans have considerable financial responsibility, if they can’t foot the bill, the worst thing that happens is their company goes under. That financial responsibility doesn’t disappear, it just gets passed up the ladder to Ginnie Mae, who would in turn be required to consolidate the tsunami of debt.

1.7 Trillion in outstanding loans…

It’s worth noting that American citizens, unlike the federal government, have learned from their mistakes. For a while, adjustable-rate mortgages (ARMs) were undesirable, shunned for the hand they played in the housing crisis. Over the past few years people have slowly warmed to the idea of purchasing these loans, but it’s unlikely that this will have any major effect on the economy for some time. That said, subprime lending is back up to 2006 levels. FHA loans have also taken a small dip, as quarter four of 2017 marked an increase in ‘seriously delinquent’ FHA loans in all but three states. While these things aren’t necessarily harbingers of another economic apocalypse, there’s some reason to worry. The U.S. is over 21 trillion dollars in debt, and if there is another housing crisis, it probably won’t end in a government bailout. The volatility of the housing market has been amplified to a deafening volume, and if we’re hit with another subprime mortgage crisis in the next five years, the American economy will be decimated. The dominoes are in place. The only question is: what will tip the first one?